Prediction Markets Crypto 15min up/down Polymarket/Kalshi Position Sizing: Kelly

Direct answer

For Polymarket 15-minute crypto up/down markets, use fractional Kelly at 25–50% of full Kelly because near-50/50 odds create high variance—full Kelly over-bets thin edges and blows up bankrolls fast. Size from your estimated true probability vs market price, not gut feel.

Pair sizing with profitable Polymarket strategy (2026) and Bitcoin up/down timing.

Author: Johannes Thüroff, M.Eng. | Last updated: June 2026

Not financial advice. See Disclaimer.

If you trade short-horizon crypto contracts on Polymarket or Kalshi, it is natural to fixate on the next tick: UP or DOWN, yes or no, right or wrong. That question matters, but it is not the whole story. Two traders can hold the same directional view and walk away with wildly different outcomes because they answered a second question differently — how large each position should be relative to the bankroll they are willing to lose.

This article explains why many participants feel “right” yet still lose, how variance behaves when odds sit near coin-flip territory, and how professionals separate edge from direction when they size positions. Along the way we will use Kelly-style framing in plain English (with the usual caveat that any formula is only as honest as your estimate of true probability), show two stylized UP/DOWN examples consistent with the math already published on this page, and tie the lesson back to tooling that helps you ask whether a market is closer to 50/50 or 54/46 before you decide how much to risk.

Why most crypto traders lose even when they are “right”

Most Polymarket and Kalshi traders do not lose because they pick the losing side every time. They lose because they bet the wrong size: too much per trade relative to how thin the edge is and how violent near-fair odds behave over short samples. I see this daily in crypto UP/DOWN markets, where contracts reset quickly, streaks arrive without apology, and a sizing mistake compounds faster than intuition expects.

The experience feels unfair — “I was roughly coin-flip correct” — but the mechanics are ordinary probability. When each trade risks several percent of capital on outcomes that are closer to a lottery ticket than a lock, a manageable edge can still produce unforgettable drawdowns. The remainder of this section names the retail pattern; later sections show why professionals route the same problem through edge-aware sizing instead of confidence-based staking.

The most common Polymarket and Kalshi crypto prediction market mistake

Consider the workflow many traders repeat:

- See Bitcoin quoted near 50/50 for the next interval

- Tell themselves it looks fair

- Risk about five percent of bankroll

- Copy that habit across dozens of markets

- Wonder, weeks later, why the balance trends down

Twenty losses in a row sting; fifty trades later the account can be impaired even when the narrative still feels like “bad luck.” It is not luck alone — it is geometry. Betting several percent per trial on instruments that behave like correlated coin flips invites variance to dominate whatever small skill might exist.

Why brutal swings are normal (even when they feel toxic)

When implied probabilities hover near fifty-fifty, three truths bite at once:

- Losing streaks occur without any requirement that you are “broken”

- Variance is large relative to edge

- Bankroll swings look emotional even when they are statistically mundane

Risking five percent per trade on repeated fair-ish binaries is closer to financial suicide than prudent speculation, even for someone who is genuinely a few points better than random. Probability does not adjust because confidence spikes on a fresh chart pattern.

Professionals think in edge, not direction

This is the pivot in mindset. Professionals rarely obsess solely over the slogan on the ticket. They ask different questions:

Retail framing: “Is Bitcoin going UP or DOWN?”

Professional framing: “Do I have an edge — and how large is it?”

If the edge is small — and in short-interval crypto contracts it usually is — then stake sizes must shrink to stay solvent long enough for law-of-large-numbers logic to matter. Direction without edge magnitude is entertainment; edge without disciplined sizing is fragile.

The Kelly criterion in plain English

The Kelly criterion is the piece many retail essays skip because it smells academic. Stay with it — the intuition matters more than algebraic theater. Kelly answers:

How much of your bankroll should you risk given the gap between what you believe is true and what the market is charging?

A simplified expression often used in prediction-market teaching is:

f* = (P_true − P_market) / (1 − P_market)

You do not need to memorize symbols on command. You need to internalize the implication: once market price embeds a probability, your optimal scale is a function of how far your well-tested belief diverges — not of how exciting the candle looks.

Kelly Position Sizing Chart

Worked sketch: fifteen-minute BTC UP/DOWN

Imagine you trade Bitcoin UP/DOWN for the next fifteen-minute window:

- Market odds: UP priced near 50¢, implying roughly fifty percent

- Your research: UP probability closer to fifty-four percent

- Implied edge: about four percentage points

The intuitive retail response is to declare conviction — “I like UP” — and deploy five to ten percent of the roll because the setup feels lively. A Kelly-style read on the same inputs, using the methodology already illustrated on this site, lands closer to risking roughly 2.1 percent of bankroll, not five, not “scaled to vibes,” but a deliberately smaller fraction tied to the modest edge.

Why accept what feels like a whisper of risk? Because that scale is the neighborhood where long-run growth and survival overlap: large enough to matter if the model is sound, small enough that ordinary losing streaks do not evict you from the game.

- It targets long-term geometric growth rather than headline swings

- It lowers risk of ruin versus naive flat-percent staking

- It acknowledges that short-sample losses arrive even when expectancy is positive

Why optimal sizing feels emotionally backward

Retail flows chase fast gains, spectacle, and “conviction trades.” Desk culture emphasizes compounding, survival, and repeatability. Psychologically, oversized bets feel powerful; correctly sized small bets feel pedestrian. Pedestrian is precisely how accounts survive crossing variance valleys.

Second stylized example: UP near 52¢ with a four-point gap

Another recurring shape — still illustrative, not a live recommendation — mirrors what traders see scanning ladders:

- Market odds: BTC UP near 52¢

- Internal estimate: fifty-six percent

- Edge: again near four percent

Using the same Kelly framing referenced above, bankroll risk lands near 1.8 percent rather than the oversized tickets enthusiasm suggests. Expected value per trade may sound microscopic — on the order of positive 0.072 percent per trade in the stylized arithmetic already published here — yet stacking fifty independent trades with controlled risk moves expectancy toward roughly positive 3.6 percent, and two hundred trades toward the mid-teens percent range, always conditional on the model being stable and execution staying disciplined.

That compounding path is how professionals discuss growth: small per-trade expectancy, strict sizing, repetition without blowing out during inevitable cold spells.

Why traders ignore sizing (and pay for it)

Sizing lacks glamour; spreadsheets rarely go viral; thin edges fail to stroke ego. So traders oversize, chase prior losers, tilt after streaks, and discard strategies that were mildly positive expected value but emotionally unbearable under blunt-force staking.

91% of Polymarket traders lose not because they can’t predict — but because they don’t size.

Polymarket versus Kalshi: structure differs, rule does not

The lesson travels:

- Polymarket fifteen-minute UP/DOWN corridors

- Kalshi hourly crypto contracts

Clearing mechanics and liquidity profiles diverge, yet the governing inequality survives:

Edge multiplied by optimal size determines whether you remain solvent long enough to compound.

Shorter horizons simply punish sloppy sizing faster — there are more draws per calendar week, so variance spends less time hiding.

The hardest input: knowing your true probability

Every sizing formula inherits garbage if P_true is invented from vibes. Common shortcuts — eyeballing charts, extrapolating Twitter sentiment, assuming “quoted fifty-fifty means fair” — inject optimism into the numerator and invite catastrophe.

Honest workflow separates inference from bravado: track forecasts, score outcomes, revise beliefs, and only then feed the machinery that suggests stake.

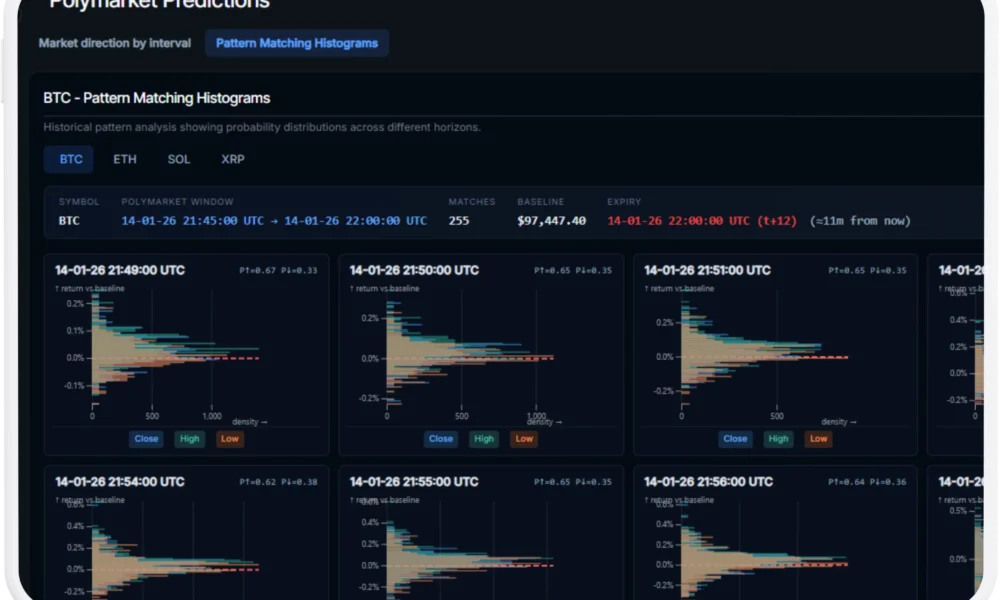

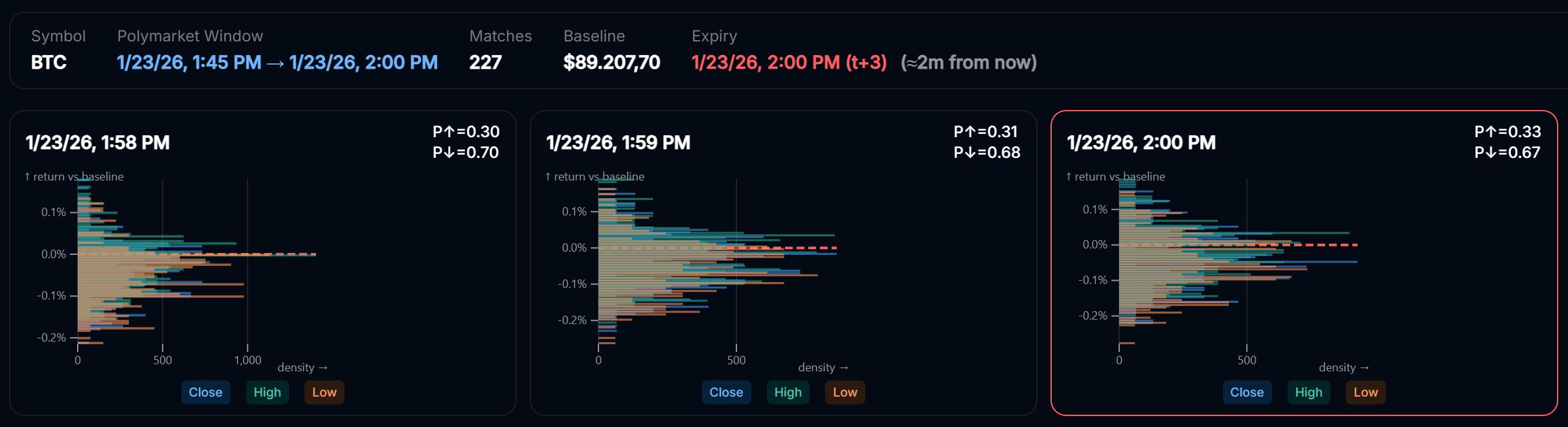

Where tooling earns its keep

Crypto is data-rich; short-horizon structure leaves fingerprints if you measure carefully. Systems that summarize historical distributions, short-term returns, and volatility regimes help expose when posted odds drift from empirical frequencies — or when late-interval drift creates conditional probabilities the headline mid ignores.

When those diagnostics disagree with the tape, you gain two actionable answers: whether an edge plausibly exists, and whether it is wide enough to justify any size above minimal curiosity capital.

How Crypticorn fits into this workflow

At Crypticorn’s UP/DOWN crypto prediction hub, the focus stays narrow: estimate realistic UP/DOWN probabilities for short-term crypto windows so traders can triangulate market prices against a structured view of uncertainty. We are not placing bets on your behalf, promising deterministic wins, or replacing your risk limits.

The objective is to equip you to answer the questions that precede responsible staking:

Prediction Markets Crypto Up/Down Probabilities Charts AI Tool

- Is this contract truly fifty-fifty?

- Or is pricing closer to fifty-four versus forty-six?

- Given that gap, how large should the trade be?

Position sizing finally connects to evidence instead of adrenaline.

Final takeaway on position sizing with crypto prediction markets

Most Polymarket and Kalshi traders do not fail solely because they lacked opinions. They fail because they swing oversized tickets at undersized edges, too frequently, without acknowledging variance.

- Betting too big relative to bankroll

- Assuming tiny numeric advantages justify hero sizing

- Repeating the cycle across correlated short-interval markets

The edge isn’t predicting better. It’s sizing better.

Pros don’t gamble. They compound.